|

This just in… Union pension proposal unveiled

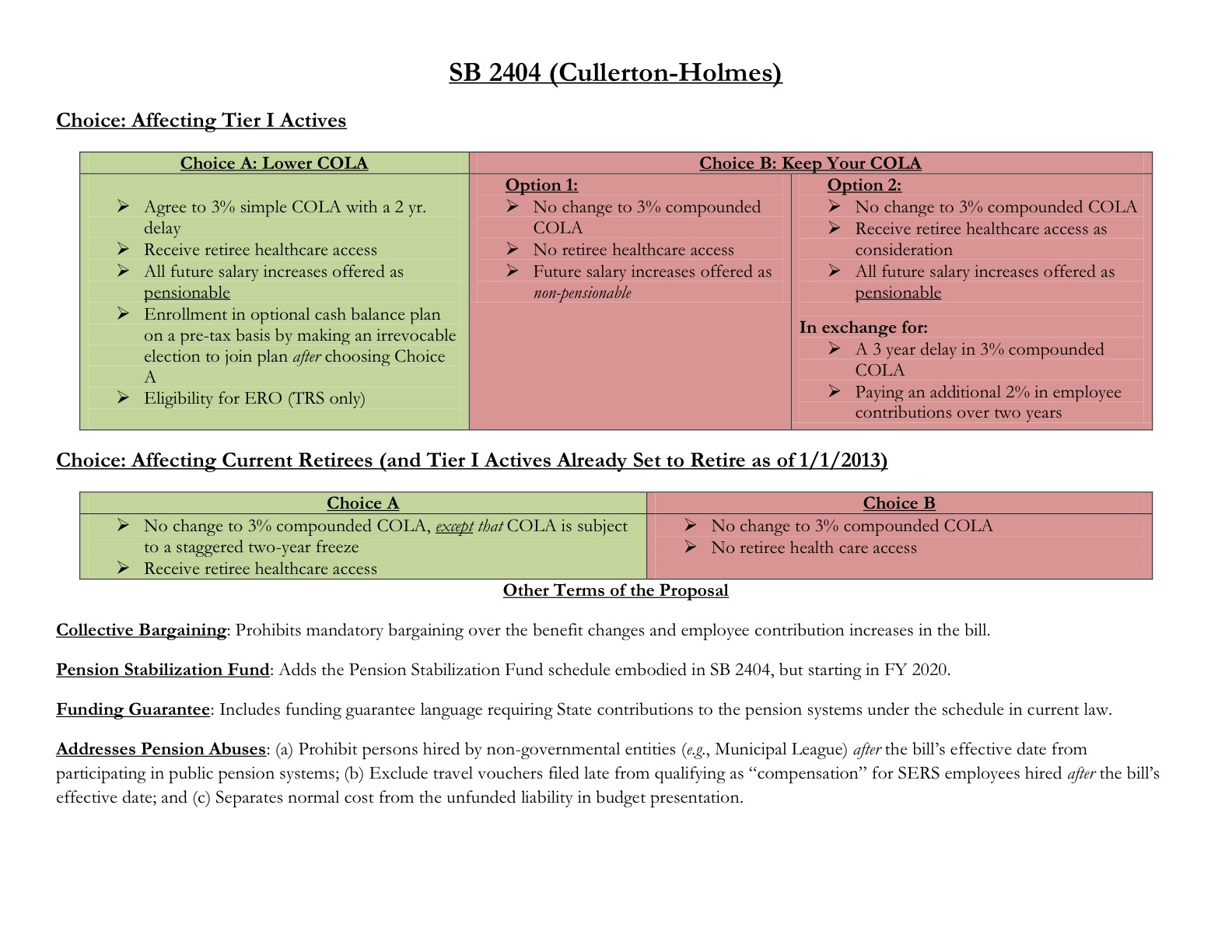

Monday, May 6, 2013 - Posted by Rich Miller * 5:16 pm - Here’s the “cheat sheet” that the Senate Democrats are using to describe union pension reform proposal. Click here or on the pic for a larger image…  More in a bit. * Senate President John Cullerton discusses the proposal with the media… * The We Are One fact sheet is here.

|

- enough is enough - Monday, May 6, 13 @ 5:23 pm:

SOS wrapped up with a new bow. No consideration because any which way you pay a whole lot more for a whole lot less. If the unions sold out for this, hope someone else takes it to court.

- foster brooks - Monday, May 6, 13 @ 5:36 pm:

put me in choice B option 2, i would then receive my cola 2 years earlier.

- boat captain - Monday, May 6, 13 @ 5:45 pm:

As a retiree I would choose choice A. At my age I could live with the 2 year freeze on the COLA and still maintain access to the state healthcare plan.

- Tsavo - Monday, May 6, 13 @ 5:46 pm:

Put me down as a choice B, I will keep the 3% COLA compounded annually and obtain my own healthcare.

- Tsavo - Monday, May 6, 13 @ 5:50 pm:

boat captain,

Is choice A staggered COLA every other year? Example, COLA in 2014,2016,etc. or is it a 2 year freeze on receiving the first COLA?

- Jesse - Monday, May 6, 13 @ 5:50 pm:

What does B 2 mean “retiree healthcare as consideration”?

- Andrew Szakmary - Monday, May 6, 13 @ 5:51 pm:

If I am reading this right, and the COLA kicks in 2 years later than it would under current law (I am an inactive member of SURS due to retire Dec. 1, 2013), then it would result in a 5.22% diminishment of the NPV of my lifetime pension benefits if I choose to keep the health care access. I don’t like this but I could live with it, and would probably not sue. But I will pursue lawsuits against Illinois to the bitter end if Madigan’s 21% diminishment becomes law.

- Mouthy - Monday, May 6, 13 @ 5:55 pm:

As it sits now I would go with option B for the already retired. My questions would be that since I had to sit the first year out of the COLAs’ does that mean I would only have an additional year to do without a COLA and does access to health care mean the formula of 2% premiums for this year and 4% for next year?

All in all, the best I’ve seen so far.

- Anonymous - Monday, May 6, 13 @ 5:56 pm:

- Tsavo - Monday, May 6, 13 @ 5:50 pm:

I have the same question? It could be a deal breaker for me??

Is choice A staggered COLA every other year? Example, COLA in 2014,2016,etc. or is it a 2 year freeze on receiving the first COLA?

- RNUG Fan - Monday, May 6, 13 @ 6:05 pm:

I wouldn’t sue over this either and I don’t think you can say the unions are not cooperative but I bet someone does sue and I have a hunch they will win, But I thought that about the original proposal.

I would describe it as annoying but not draconian

- mythoughtis - Monday, May 6, 13 @ 6:06 pm:

I would select B, option 2. FYI - employee with six years of service, expect to work 8 or so more. I don’t mind a hike in employee contributions, and a short COLA freeze makes more sense to me.

- Arthur Andersen - Monday, May 6, 13 @ 6:06 pm:

Hmmm. Choice A. About a 5% haircut plus healthcare increases. Could be a lot worse.

I’m still working through how this saves more dough than Mr. Speaker’s bill. Devil in the details.

- Michelle Flaherty - Monday, May 6, 13 @ 6:07 pm:

I believe the two-year staggered COLA means one year you dont’ get it, next year you do, following year you don’t. Intended to spread the sacrifice.

You’d be giving up two COLAs over a three year period.

- RNUG - Monday, May 6, 13 @ 6:14 pm:

Been busy all day. Need to find time to read the actual bill tonight but the summary doesn’t impress me.

- enough is a enough - accurately summed it up.

- Mouthy - Monday, May 6, 13 @ 6:17 pm:

This is also a “gift” to the high end pensioners as if they go for Option B then they don’t lose the two years of COLAs’ but instead use them for insurance premiums and continue to compound their pensions unfettered.

- Arthur Andersen - Monday, May 6, 13 @ 6:20 pm:

RNUG, I don’t think they have posted their proposal in bill form yet unless I read it incorrectly.

- huggybunny - Monday, May 6, 13 @ 6:28 pm:

isn’t the healthcare issue still being decided by the courts? How can healthcare be a consideration tied to pension reform, if the courts could decided health care was a contract and members are entitled to it?

- WOW - Monday, May 6, 13 @ 6:32 pm:

Mouthy, you are right. It would help the high enders. Especially the ones on medicare.

The “staggered” terminology has everyone a bit confused.

And we all know that some will say it is not enough.

- iThink - Monday, May 6, 13 @ 6:37 pm:

Any idea what the cash balance plan would be for Choice A?

For active workers who aren’t very near retirement, Choice B, option 1 is a terrible choice.

I like these a whole lot better than what has been put out by MJM, but still not certain how this is constitutional, but I am sure Cullerton knows better than I.

For you teachers out there that my be enticed by the ERO option in choice A, remember that is a bargained item with your district as they pick up a large part of the fee. That fee is due to increase substantially due to a change in actuarial method. Just don’t take it as a given.

- Bill - Monday, May 6, 13 @ 6:37 pm:

This is not a bad compromise! It hurts but consider the alternatives.

- iThink - Monday, May 6, 13 @ 6:43 pm:

I would really like to see the details on the stabilization fund to make sure it’s just not a kick the can down the road.

- Arthur Andersen - Monday, May 6, 13 @ 6:48 pm:

Bill, well said. People have to realize that the status quo is not sustainable.

- Bill - Monday, May 6, 13 @ 6:49 pm:

AA,

It saves more money than the Madigan bill which will save nothing when its declared unconstitutional by the courts.

- Bill - Monday, May 6, 13 @ 6:51 pm:

Depending on your personal choice and situation you’re looking at a 5-10% decrease in lifetime benefit as opposed to 20-30% in the Madigan bill.

- RNUG - Monday, May 6, 13 @ 6:51 pm:

AA,

I just assumed a draft was out there in a shell bill … but the amendment may not be filed yet. I’m just getting caught up on the day.

For what it’s worth, based on just the chart, I’d pick B. I’m basing that choice on several things, including age and financial impact, but here’s the main point: when this is eventually found unconstitutional, it’s going to be a lot easier to have the health insurance restored than it will be to undo what the IRS may view as an irrevokable pension modification.

- cassandra - Monday, May 6, 13 @ 6:56 pm:

It gives more choices to cover what must be a variety of different retiree situations. That’s a good thing.

The stronger language on pension payments might head off future runs on retiree benefits. But it’s not a sure thing.

It’s still a diminishment. Don’t forget that. The underlying premise is that retirees present and future should pay for some very bad mistakes by Illinois politicians and their appointees. And once retired, even if the economy takes off again, which it almost certainly will, they won’t get it back.

- RNUG - Monday, May 6, 13 @ 7:02 pm:

huggybunny @ 6:28 pm:

Yes. The Nardulli ruling in the consolidated Maag case (no protection under pension clause, no contract) is on appeal to the IL SC but we probably won’t know anything until fall.

There is also the Appellate Court order in the Joliet v Marconi case (skip back a couple of days to Skeetyer’s posting to find a link). They said the trial level “protected under the pension clause” decision was incorrect because there was no need to go to the pension clause, it should have been decided under contract law. They issued an order to the lower court to reopen the case based on contract law, directing it should be assumed a enforcable contract exists unless there is contrary written proof.

So there is a clear difference of opinion in the legal system … and until we get the IL SC opinion, these “choice” options are questionable.

- RNUG - Monday, May 6, 13 @ 7:06 pm:

Whether the pension guarantee is worth the paper it is written on depends on which version gets incorporated in the union / Cullerton bill. The Madigan version is a waste of ink; it can be easily circumvented by future GAs. Some of the other versions read like they might be able to be partially enforced.

- cassandra - Monday, May 6, 13 @ 7:11 pm:

And I think the state is going ahead and charging retirees for their health insurance premiums starting this July, right?

- Anonymous - Monday, May 6, 13 @ 7:11 pm:

I’m going to need a pension expert to explain all of this. I’m hoping that current non-retirement employees won’t have to make decisions on this until we reach retirement age (I really din’twant to decide now what plan I want to be in in another 15 years). Cullerton mentioned in the video that the Union wouldn’t sue since this is their plan, but I assume non-union employees not represented by the union would still bring a suit.

- RNUG - Monday, May 6, 13 @ 7:13 pm:

Everyone who says they would opt for the option with health insurance, remember that is just ACCESS to be able to BUY the health insurance.

The only time that is really worth anything is if you are under Medicare age and you have pre-existing conditions … and the ACA is supposed to fix that problem.

- RNUG - Monday, May 6, 13 @ 7:14 pm:

cassandra @ 7:11 pm

Yes, that is the current plan according to the paperwork I have received.

- Anonymous - Monday, May 6, 13 @ 7:14 pm:

I’m confused. Okay — this looks far, far better than the Madigan plan. So, okay — let’s say it passes. Then what?

Wait a year — and Madigan re-introduces another plan? Maybe that looks better next year because the fiscal situation is worse. That passes. Then what?

Two years from now, Madigan introduces another plan. “We need to do it. The fiscal situation demands it. We have no choice.”

In other words — what’s the point of supporting anything? Whatever passes this year will be tweaked next year. Made more extreme. The year after — even more extreme. It’s an endless cycle. It doesn’t matter what “passes” because everyone is always gonna hammer at it until the actives and retirees get as close to nothing as possible.

So this passes. So what?

- huggybunny - Monday, May 6, 13 @ 7:21 pm:

RNUG @7:02 p.m.:

Thanks for the clarification on the court case. One other question, it says for (Choice: affecting current retirees (and Tier 1 Actives already set to retire as of 1/1/2013) Does that mean actives who turned in paperwork with their retirement date listed or also actives who have had a retirement counseling session before 1/1/2013. Think I’m out of luck on this one.

- Norseman - Monday, May 6, 13 @ 7:32 pm:

MF thanks for the insight. Your interpretation makes sense in that it would save more money. Unfortunately, it would make Choice A less desirable.

- Roadiepig - Monday, May 6, 13 @ 7:33 pm:

As a retiree I have to wonder how the “B” choice option would be implemented if the Supreem’s go with the retirees in the Magg suit. No choice option for current retirees should be offered until that has been decided, because once a choice is made the retiree has agreed to a new contract. If I take option A (alternate formula retiree with several pre-existing conditions)I would have my COLA cut, and retirees who took option B would lose nothing if the courts decide the health care was a contract.

- WizzardOfOzzie - Monday, May 6, 13 @ 7:51 pm:

Bill,

Please explain to me how these two things are consistent with each other.

- Bill - Monday, May 6, 13 @ 6:49 pm:

AA,

It saves more money than the Madigan bill which will save nothing when its declared unconstitutional by the courts.

- Bill - Monday, May 6, 13 @ 6:51 pm:

Depending on your personal choice and situation you’re looking at a 5-10% decrease in lifetime benefit as opposed to 20-30% in the Madigan bill.

So a bill that only decreases by 5-10% is going to save more than one that decreases them by 20-30%? I’m not saying your wrong, but I have a really hard time believing that.

- RNUG Fan - Monday, May 6, 13 @ 7:56 pm:

RNUG

You may not want the salary freeze If you have a lot more salary then its option 2 and the health care access is a small bonus….In the end its pay more for what you get and its a diminishment just not a draconian one

- RNUG Fan - Monday, May 6, 13 @ 8:02 pm:

Anon

Even a union employee could sue on their own. I know one retired lawyer who I am sure will.

If you can show harm you can usually have access to the courts

- Arthur Andersen - Monday, May 6, 13 @ 8:20 pm:

Wizzard, I agree with Bill and we are basing what we say on the figures calculated by the actuaries. The math is extremely inside baseball and I’m not sure if I fully understand it yet.

For example, the Cullerton plan requires 90% funding while Madigan takes us to 100%. By spending less money to only reach 90, is Cullerton “saving more?” Madigan also changes a complex actuarial assumption that could involve billions in added costs; Cullerton doesn’t.

Reasonable people could argue about going to court on the Cullerton plan. I haven’t heard anyone who won’t fight the Madigan plan tooth and nail.

- Former Merit Comp Slave - Monday, May 6, 13 @ 8:23 pm:

SB 2404……I’m still very wary of any choice until Maag is decided. My toes are getting tired of hanging over this cliff. Set to retire in less than 3 months……

- kimocat - Monday, May 6, 13 @ 8:25 pm:

OK, where do non-active SERS members end up? It certainly doesn’t seem that we can take advantage of provisions for actives since we are no longer employed by the State.

- RNUG Fan - Monday, May 6, 13 @ 8:42 pm:

The SJR has a good report on this. It says Sen will NOT vote on Madigan again but Madigan Nekritz still needs to be fought politically.

It goes to Sen Exec Wed and passes Thurs anyone want to guess the margin?

How will Madigan respond?

- Makandadawg - Monday, May 6, 13 @ 8:43 pm:

I have been eligible to retire the past two years still waiting to earn my maximum benefit. Now Cullerton wants to tell me I should have retired 5 months ago?

- RNUG Fan - Monday, May 6, 13 @ 8:59 pm:

No they get to join us in a COLA Freeze BTW SJR says its just a 2 year freeze. It was not clear in the chart

- Living in Machiaville - Monday, May 6, 13 @ 9:01 pm:

So…..which is it….the red pill or the blue pill? hmmm?

- The Whole Truth - Monday, May 6, 13 @ 9:12 pm:

I believe Anon 7:14 has it pegged. What parts of either Madigan’s or Cullerton’s bills makes them any more “contractual” than the Constitutional provisions already in place? What keeps this same type of take-back from happening again and again? Once the precedent is set, there’s no going back, and no pension “contract” is worth the paper it’s printed on. Wonder which contracts will be next?

- RNUG - Monday, May 6, 13 @ 9:14 pm:

huggybunny @ 7:21 pm:

I don’t know but that would be my guess …

- RNUG - Monday, May 6, 13 @ 9:20 pm:

R-Fan

Maybe I didn’t make it clear, but I was speaking of my personal situation … I’ve been retired since the 2002 ERI at a fairly high pension (which shouldn’t surprise any regulars b/c I’ve admited to being a retired SPSA).

- Vitaman - Monday, May 6, 13 @ 9:24 pm:

huggybunny @ 7:21 pm:

What prevents you from turning in a one day notice of retirement if you are eligible?

- huggybunny - Monday, May 6, 13 @ 9:49 pm:

Vitaman @ 9:24 p.m.

What prevents you from turning in a one day notice of retirement if you are eligible?

I’m eligible to retire, have just been waiting to see what they take away so as to know how much I’ll have to live on. Think I’ll make my phone call tomorrow to see about it, don’t want to give just one day notice, but they may have left me no choice. Hard to know what’s the right choice with the health care decision still being determined by the courts. Nothing like making a life decision with only some of the facts.

- Crossface - Monday, May 6, 13 @ 9:49 pm:

Does this mean those who retired at age 55 will still receive their retroactive COLA payments at age 61?

- Oh boy! - Monday, May 6, 13 @ 9:49 pm:

So what is a two year freeze? I have been retired 6 years and expect to get my first cola of 18% in February. What is status of that with this bill?

- No-raise - Monday, May 6, 13 @ 10:41 pm:

Union is very reasonable and the Tribune should take notice. Sick and tired of everyone dumping on government employees. Ten years ago, all I heard was “why don’t you get a real job and makes some real money?” Suddenly, the economy tanks and now those same people want to take away our hard-earned benefits. Well that’s why we stuck it out instead of making “real money.” Too bad.

- Norseman - Monday, May 6, 13 @ 10:41 pm:

The We Are One fact sheet that Rich posted is helpful. If we could trust this would be the extent of the so-called shared sacrafice, this wouldn’t be a horrible plan. Unfortunately, we can’t trust that this is the end of the reduction of benefits. The problem with this bill is that it lays the groundwork for future reductions of public worker pension benefits.

If this bill passes and is upheld or unchallenged in the courts, I can only hope I die before the next round of cuts come.

Of course, passing is going to be the big “IF” for this proposal. I’m sure it doesn’t cut enough money to satisfy the one-percenters and fire-eaters to the right. The Speaker may also throw one, or many, monkey wrenches into the mix.

- RNUG - Monday, May 6, 13 @ 10:55 pm:

It’s my guess they set the “notice to retire” for active employees at an already past date, 1/1/2013, in order to prevent another rush for the exits like last year … when they suffered yet another brain drain because the GA scared a lot of people out the door. Either that or it’s to cover the teachers that have to give irrevocable notice a year or two in advance. I think for most people, it’s too late if the date in this bill is enacted.

- huggybunny - … I don’t know what system you are in (you probably can’t do this as a teacher since that election has to be irrevocable), but I would inquire if you could turn in an intent to retire now and revoke it later should you decide to stay. I know under the SERS 2002 ERI you could tell them you intended to retire but it didn’t actually take effect until you turned in a real resignation letter. Language such as “subject to future written revocation, it is my intention to retire 12/31/2013″ or words to that effect. That might let you hedge your bets should a different date be passed in some bill. If possible, the only down side I can see to such an action would be you might get passed over for a raise if your employer thinks you are leaving.

- RNUG - Monday, May 6, 13 @ 11:18 pm:

FYI … the SJ-R is reporting the bill is SB2404. I just looked at it and the current language is just the funding guarantee at 100%, none of the revised language is in there. Since Cullerton is one of the sponsors, it could still be the shell bill that gets used …

- huggybunny - Monday, May 6, 13 @ 11:21 pm:

RNUG @10:55 p.m.

Thanks, I appreciate your responses. I will definitely check into it tomorrow.

- Mouthy - Monday, May 6, 13 @ 11:35 pm:

Good Cop / Bad Cop

So Madigan scares with his bill

Cullerton says hold the fort, I’m working with the union.

Presto, union plan comes to pass.

Whew, says everybody, that plans’ not too bad, it could be a lot worse.

If I had a best guess I’d say Madigan, Cullerton, and the union leaders have had this all worked out to get a bill passed while providing cover to the unions. I’ve seen this movie before.

You all don’t think this is really a legit p’ing match between Madigan and Cullerton do you? Say it ain’t so…

- huggybunny - Tuesday, May 7, 13 @ 12:28 am:

So what happens if we voluntarily give up the right to access to health care, and then the Supremes rule health care is guaranteed per our contract? How can we be forced to decide to give something up when it’s still being decided by the courts? We’re being forced to make a decision when we don’t have all the facts.

- foster brooks - Tuesday, May 7, 13 @ 5:51 am:

I’m sure the IPI , civic federation, commercial club and GA republicans will jump aboard this plan.

Lol

- RNUG - Tuesday, May 7, 13 @ 7:25 am:

huggybunny @ 12:28 am:

I can’t tell you right now what the language in the latest bill will be because it didn’t seem to be out there last night. But the previous Cullerton choice bill, when you did not make a choice, had the ‘default’ be to retain the existing COLA terms and lose insurance access … which is recognition of the protected status of the COLA.

FYI - my mom spent some time on the phone with the CMS insurance people the other day. Because a lot of this is up in the air, they don’t have too many firm answers either. They seemed to be just as frustrated as the rest of us.

- DoubleD - Tuesday, May 7, 13 @ 7:34 am:

Regardless of whatever will pass…can we include an amendment for term limits as part of the package because every lawmaker who has been around for the long haul created this mess and deserves to be held accountable. The option I want is the ability to put all the irresponsible legislators back in the workforce.

- boat captain - Tuesday, May 7, 13 @ 7:45 am:

@ RNUG-I choose the option A as a retiree because I don’t trust the courts to rule that health insurance is a protected benefit. I see your logic about the default option that they think that the health ins is a protected benefit. I can live with the two year COLA freeze and get the 3% compounded raise thereafter and still have access to the state insurance plan. I would rather pay a percentage of the health insurance premium than have to pay the whole thing. I am not at medicare age. Am I reading this or seeing this wrong?

- boat captain - Tuesday, May 7, 13 @ 7:49 am:

@ RNUG-Meant to say they think that the cola is a protected benefit.

- RNUG - Tuesday, May 7, 13 @ 8:12 am:

boat captain,

I think you’re seeing it straight for your situation, given your assumption.

If we are forced to make one, the “right” choice is going to depend on a person’s age, health and the need for dependent coverage also.

The biggest problem with the health insurance access is you are buying a pig in a poke. There is no guarantee what the rates will be. If you believe some of the predictions floating around the health care industry, insurance premiums may as much as triple in the next year or two … and it’s my feeling the State will try to pass every bit of any future increase on to us.

My logic would be, if possible, to take the default (by not making a choice and letting it default). That would let me retain the legal argument I did not make a choice. But, unlike you, I expect the courts to eventually find that TRS /(some) SURS have a contractual right to insurance access by virtue of their pre-payment to the insurance fund and I also expect the courts to find that SERS / JRS / GRS / (some) SURS have a contractual right to free health insurance if they put the 20 years in. Time will tell.

Anyway, until there is actual language in a bill, we are just guessing. Ideally, given the need to hold a choice period, there may be a final court ruling before we have to make a choice.

- WOW - Tuesday, May 7, 13 @ 8:14 am:

Is this plan just “kicking the can” down the road.

Cullerton said it would free up money for education. Shouldn’t the saved money be applied to the pension debt. This is like stealing from retirees again. USE THE SAVED MONEY TOWARDS THE PENSION LIABILITY.

Or maybe the union should call Madigan’s bluff and let the Supreme Court decide once in for all.

We all know with this plan we will be back at the table in a few years and they will want to rob us again.

Looks like this plan was laid out by the Democrats and Unions last year. You can’t trust any of them. They have manipulated us once again.

- RNUG Fan - Tuesday, May 7, 13 @ 8:32 am:

I would almost believe Mouthy but

Madigan and Cullerton have had this disagreement on the Pension and Constitution for years

Madigan and AFSCME have been at odds for a long time

Boat capt. Your health costs should be determined by the AFSCME contract which is not yet a done deal Since its 3 Years retirees should have the info to make their decision

- boat captain - Tuesday, May 7, 13 @ 8:53 am:

@ RNUG-Thanks for your input-I too believe that the health ins benefit is protected but am unsure at this time how the courts will rule. Hopefully there will be a court decision before we have to decide so we can make a choice that will work for us individually. I, as you believe that the premiums will go up in the future and the State will pass them on to us. Thanks again.